Low-code/no-code

Among the major TMT sector trends, we heard that low-code and no-code customer adoption within enterprise IT is in its early innings. Low-code is used to build tools to accelerate existing developer productivity, while no-code use cases disintermediate skilled developers. A former executive at Quickbase Inc said the low-code market is growing at 10- 20% YoY, with a global TAM opportunity in the “double-digit billions”.

No-code could experience 30-50% YoY revenue growth over the next five years as citizen development increases, and the industry could consolidate rapidly over the next 1-3 years as large-scale SaaS franchises pick off players who fail to reach critical mass, according to the Interview.

Supply chain software

Having been a “stagnant industry” for a long time, the importance of supply chain management (SCM) is becoming increasingly apparent in the aftermath of COVID-19. A shift from just-in-time delivery to a more agile approach, as well as labour constraints, are among the major drivers of investments and innovations in the supply chain software space.

A former VP at Blue Yonder Group Inc sees SCM industry TAM at around USD 30bn, with a CAGR of about 10% over the next five years. SCM solutions can be categorised primarily as planning, representing 30% of industry revenues, execution (50%), and collaboration (20%). Around a fifth of revenues come from cloud solutions and this could rise to half within three years, reflecting a current upgrade cycle and demand for modern and integrated solutions, according to the Interview.

European football leagues

There has been a renewed interest from PE in European football leagues, chasing stake investments in domestic and international audiovisual rights. Bundesliga, LaLiga and Serie A have been topical this year. As reported by various media outlets in September, Bundesliga has been in talks with buyout firms about a multibillion-euro investment. A former divisional leader at Bundesliga International GmbH (DFL Deutsche Fußball Liga GmbH) told us that although clubs have historically rejected PE investments over fears of losing control, financial pressure is building, with the expert citing a 20% increase in salaries and agency fees in recent years.

We heard that domestic media rights stakes are likely suited for domestic PE funds, and that international media rights valuations and revenues are linked to national team and club performances. The expert valued domestic media rights at approximately EUR 1.1bn per season vs international rights of about EUR 165m per season (50-70% of the latter coming from the EU, followed by Americas and Asia). Bundesliga’s international media rights are likely to increase, driven by German clubs’ increased overseas audience engagement, touring and marketing. LaLiga, while already invested in by PE, has a significant credit issuance, while Serie A is currently looking for investments by PE for its media rights.

English and European football clubs

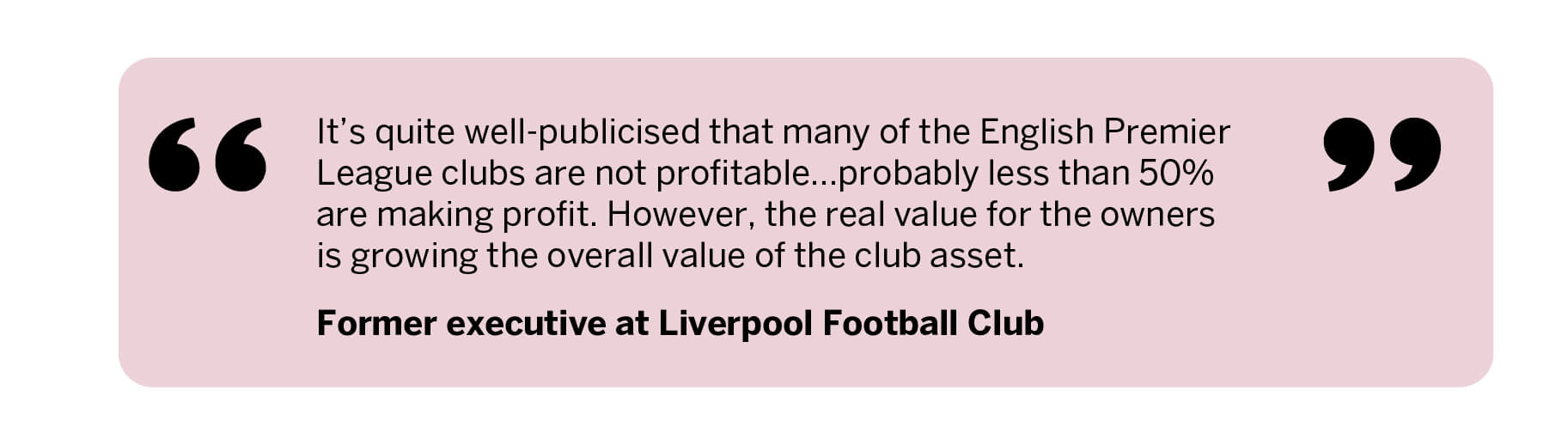

PE houses and investment consortiums have also been busy scoring deals with English and European football clubs including Chelsea, Barcelona, Real Madrid, AC Milan and Olympique Lyonnais, with Liverpool FC now seeking a new investor. In an Interview on investment in English football clubs, a former executive at Liverpool Football Club told us that it is “substantially much more appealing” for private capital firms than clubs playing in other leagues across Europe. They told us this is due to the “prize” of significant broadcast revenue and the “global exposure or appeal” of the English Premier League brand.

Although only about half of current English clubs are profitable, the specialist believes that the real value for owners is in growing overall asset value. Clubs that could suit private financing include West Ham United and Crystal Palace, given their London location. Private financing could also be used to redevelop stadiums to increase capacity and match day offerings, which they said could increase turnover, with most clubs “oversubscribed” with fans. Similarly, Italian, Spanish and French clubs have also been scoring investments. Our experts have laid out the different constraints limiting the financial health of these clubs and opined on different strategies to diversify revenues and drive audience engagement.

Gaming

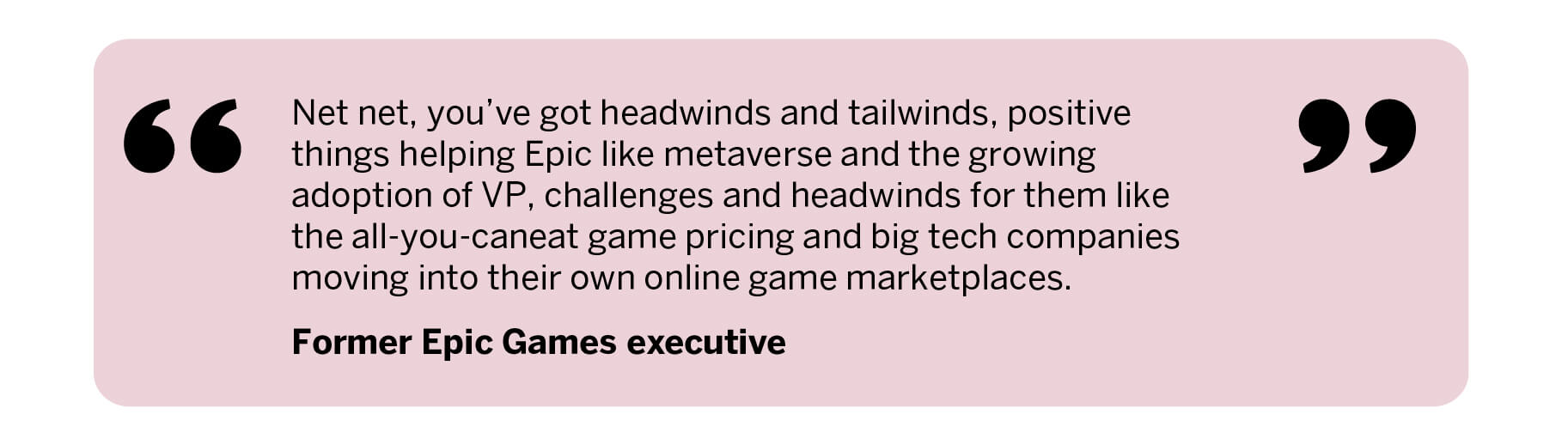

The COVID-19 pandemic ignited a period of exceptional growth in the gaming sector and as we look to the future, the landscape is being further shaped by opportunities as well as challenges. The metaverse was cited by a former Epic Games executive as a “whole new opportunity for game development companies”, enabling them to extend the life cycle of popular games and interact with users in new ways – improving retention and creating new revenue streams. Virtual reality (VR) is also enabling companies to create more immersive games and is becoming more accessible thanks to improved CPU capacity and falling costs of hardware.

Industry headwinds, we heard, include monthly subscription models with PC gaming companies, which allow users to flit between games and can therefore reduce loyalty and harm ARPU. On the other hand, this presents a new revenue stream for the industry more broadly. Another challenge is big tech players creating their own gaming marketplaces and thus increasing competition. Lastly, the impact of a recession on ARPU is yet to be seen, and the Great Resignation could also push up industry salaries as companies seek to retain talent.

Web 3.0 in China

Concepts such as decentralised social platforms and the metaverse have given stronger impetus to Web 3.0, the third generation of the World Wide Web that distributes data on networks through blockchain technology. As we heard from a former SVP at a bitcoin mining company in China, Web 3.0 development in China is among the slowest globally and is not expected to play a role in its financial industry – but could replace Web 2.0 in certain scenarios such as social platforms, e-commerce platforms and network services.

We also heard it is “impossible” for any single player to monopolise the Web 3.0 market, which will ultimately consist of various enterprises that provide underlying public blockchains, applications, cross-chain technologies, as well as blockchain management services. “No single player can dominate or monopolise the business,” the specialist said. “Otherwise, it may run counter to the concept of decentralisation.”

Terra, Solana, Fantom and other public blockchain platforms developed overseas have their own capabilities including in transactions, NFT trading, asset management and mortgage application. Overall, the expert predicted that Web 3.0 milestones will be reached in 2024/25, citing the widespread uncertainties regarding the future of Web 3.0 generally and today’s macroeconomic headwinds compounding this. Indeed, companies investing in Web 3.0 are “casting their net wide” because it is impossible to know what the leading technology, business model, and regulatory landscape will look like.

Click here to access the full report, Private equity themes of 2022 and beyond.

Related Transcripts

Web 3.0 in China – Ecosystem & Development Trends

Low-code & No-code App Development Sector Update – H2 2022 Outlook

Deutsche Fußball Liga – Bundesliga Media Rights Sales Structure & Monetisation Opportunities

Epic Games – Unreal Engine Update & Q3 2022 Outlook

Supply Chain Software – Q4 2022 Update – Blue Yonder, E2open, Manhattan Associates & More

English Football Clubs – 2022 Operating Landscape Update & Take-private Considerations

The information used in compiling this document has been obtained by Third Bridge from experts participating in Forum Interviews. Third Bridge does not warrant the accuracy of the information and has not independently verified it. It should not be regarded as a trade recommendation or form the basis of any investment decision.

For any enquiries, please contact sales@thirdbridge.com