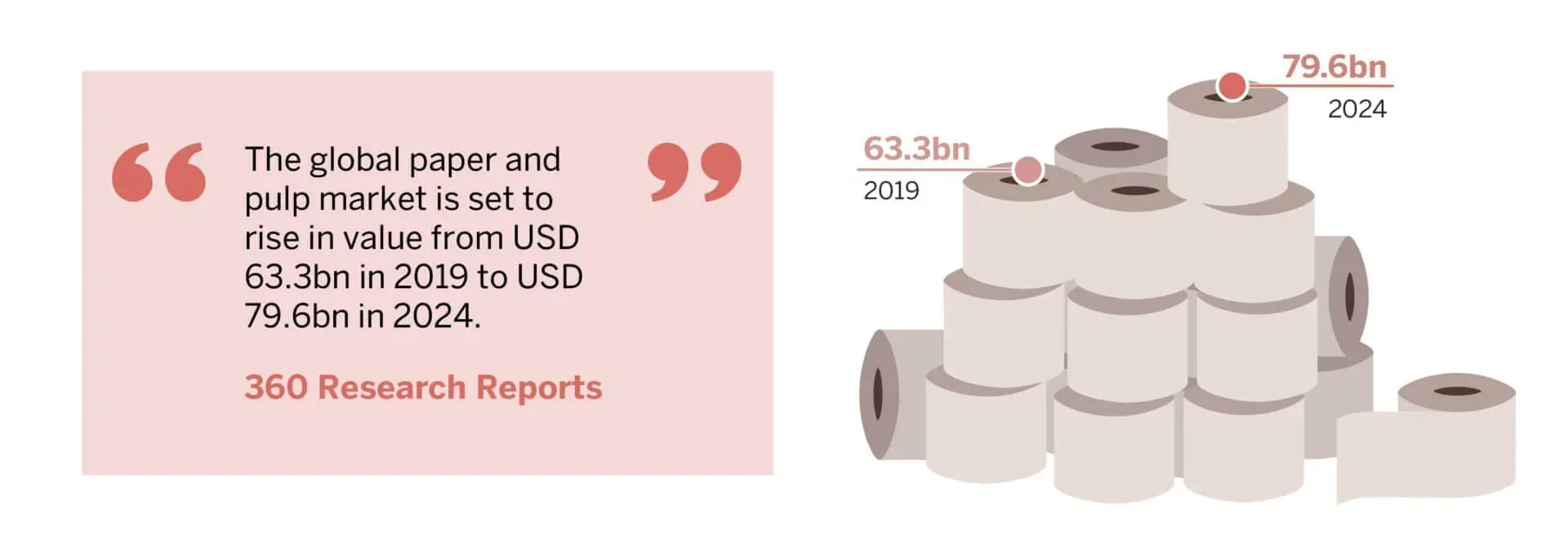

The global pulp industry has been through the mill somewhat in recent years against the backdrop of price fluctuations, the US-China trade war and inventory overhangs. After a run-up on price, demand started to tail off for market pulp YoY for the first time in a long time towards the end of 2018. Although an ensuing price correction led to renewed demand, particularly for softwood, a significant inventory overhang in hardwood remained the focus of 2019.

Although suppliers had anticipated a weaker Q1 2020, there was some positive news for the industry as the eucalyptus overhang in China was brought back down “to at least the high side of the normal range”, a specialist told Third Bridge Forum. “Softwood in particular had been much better in balance.” As a result, the industry felt more optimistic about how it would fare after Chinese New Year. But the COVID-19 outbreak and ensuing China shutdown had, and continues to have, notable impacts on global pulp market dynamics. As noted by the aforementioned expert, “all eyes are always on China” when it comes to global demand for pulp. “It leads the globe from a pricing sentiment and a price actualisation perspective.”

With containers and vessels at a standstill in China for weeks, shipping capacity and container availability dropped in North America, China’s main source of pulp. Then, just as China was able to emerge from its lockdown, with manufacturing and demand starting to pick up again, the outbreak intensified across the US and Europe, with “pretty intense [pulp] shortages” anticipated through April and into May.

Meanwhile, the industry has been dealing with a huge spike in demand for consumer tissue, which could exacerbate supply and demand issues once people stop stockpiling. The away-from-home tissue sector is “a big question mark” and risk area, though, given the volume of cancelled events and hotel and restaurant closures. “That sector is probably going to be hit harder than the consumer sector as you look forward,” the specialist said. However, because the away-from-home market uses more recycled pulp than the consumer tissue market, “it’s going to have a bigger effect on the recycled side of things, meaning less demand for deinked or reclaimed fibre”. About 70% of away-from-home tissue is made with recycled pulp whereas 90%-plus of consumer tissue is made from virgin fibre. To cope with these changes in demand, there is some “marginal swing capacity” for tissue manufacturers to temporarily shift their focus from away-from-home to consumer products. Indeed, three of the critical manufacturers in Hubei province that were allowed to resume production after the lockdown were in the tissue business.

Heightened demand for tissue and hygiene products could be offset by waning demand in the printing and writing sector. Order volumes of high-quality kraft cardboard paper and coated white cardboard in China have “declined significantly” because of dwindling demand overseas, with a “big rebounce” not expected until June, July or August. High-quality kraft cardboard paper is used for mobile phone packaging and other electrical appliances. It’s expensive because it’s made of wood pulp, and most of the wood pulp in China is imported, another expert noted.

Recent pricing volatility in North America has helped to buttress the low side and create opportunities on the upside. “This is one that as a manufacturer everybody wrestles with, you don’t want to look tone-deaf but at the same time things are going to cost more to get product from point A to point B, whether it’s a staffing situation, a supply chain situation, all of those types of thing,” one of the aforementioned experts said. “It’s unrealistic to expect that that just falls on any one point in the value chain.” Two North American suppliers of northern softwood “that were here two months ago” are no longer manufacturing pulp, he added; one is a permanent closure and the other temporary (30 days) owing to fibre supply issues.

The global pulp industry entered 2020 anticipating a potential price uplift, but like many other industries, has had to adjust its outlook. Whether there is scope for pricing upside in the long term could depend on factors including government stimulus packages and short-term loans. When China lifted a tariff on US recycled paper pulp shipments, for example, “that had an immediate effect on southern softwood going into China”. Suppliers also need to “protect the customers that have been with them through thick and thin”, which can be done by elevating prices in order to sustain operations and suppress speculative demand. “That to me translates into upside pricing opportunity even in the shorter term to mid term,” the expert said. “Not a dramatic spike or run-up, but something that takes it off of where it is.”

The information used in compiling this document has been obtained by Third Bridge from experts participating in Forum Interviews. Third Bridge does not warrant the accuracy of the information and has not independently verified it. It should not be regarded as a trade recommendation or form the basis of any investment decision.

For any enquiries, please contact sales@thirdbridge.com