In recent weeks, Third Bridge Forum has heard that a number of E&C players are shying away from oil and gas and turning their attention to bright spots in other end markets. We interviewed a range of experts, including a former senior manager at Fluor Corp, former EVP at KBR Inc and former C-level executive at Jacobs Engineering Group Inc, to discuss some of the challenges and opportunities facing the E&C industry.

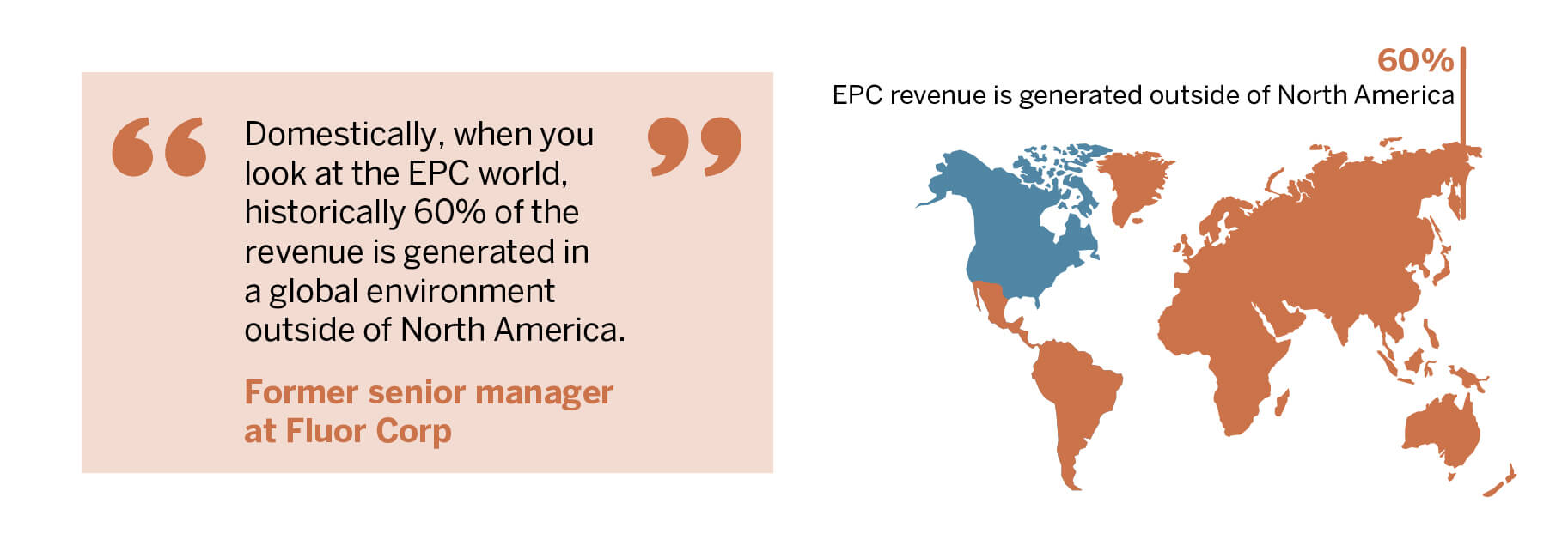

In recent years, 60% of US engineering, procurement and construction (EPC) revenue has been generated outside North America, we heard in one Interview. At the same time, competition in the global market has intensified, resulting in tougher bidding processes and a shift from the cost-plus to fixed-cost model. This has left larger E&C players wrestling with the significant risks of fixed-priced work, particularly in oil and gas, where costs can quickly spiral. Compounding this, knowledge transfer from project to project is awkward, and fast-moving technology can make it difficult to rely on previous bids and estimates. As a result, firms are moving away from the fixed-cost model while trying not to lose projects to competitors willing to adopt that contract structure.

More recently, Forum Interviews suggest E&C players are also seeking to stabilise their revenues by targeting more reliable end markets, such as government services and engineering, procurement and construction management (EPCM) work. For example, KBR is “moving on from the old days of oil and gas” and refocusing on a “more sustainable reimbursable model”, a former EVP at the company said. Government services markets are large and diverse, with an abundance of opportunities to acquire companies and grow organically. KBR’s acquisition of Centauri, which provides engineering and development solutions for national security missions associated with space, intelligence, cyber and emerging technologies, is a recent proof point. The move reflects KBR’s desire to provide digitally enabled solutions and technologies in stable domains, its CEO said.

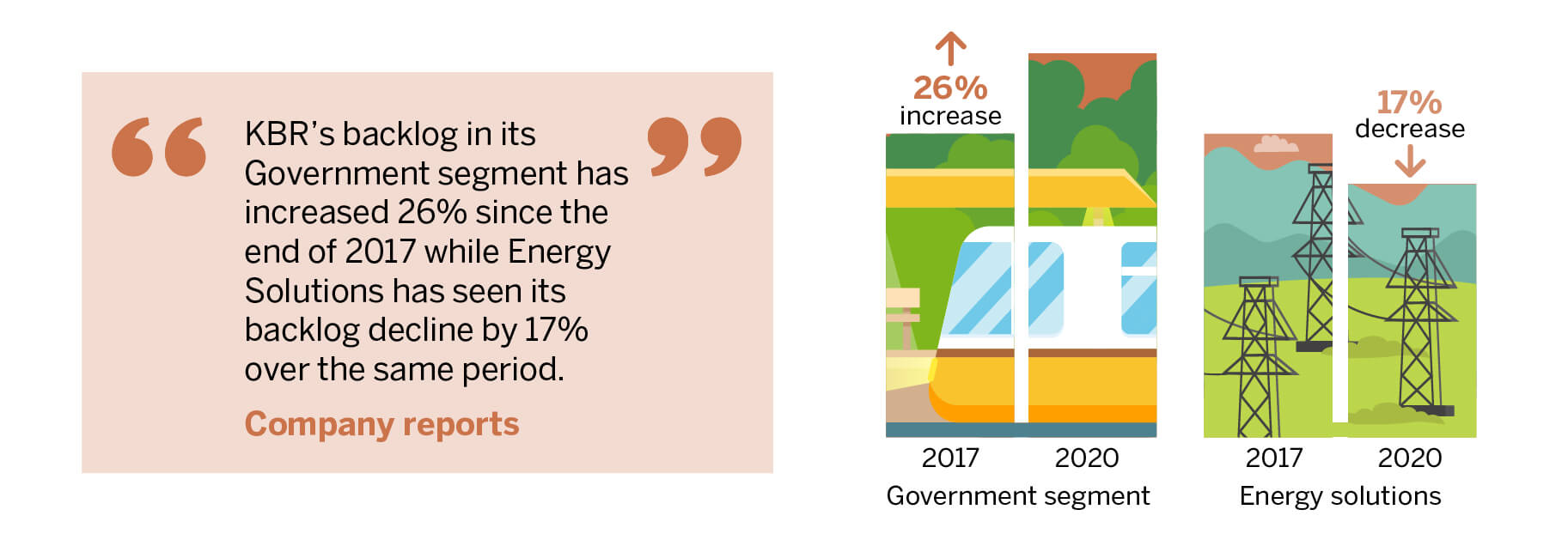

“At the moment, there’s a drag caused by this continued exposure to the energy industry in very uncertain times,” the former KBR EVP added. But the company is not alone on this front. “We still see companies like Fluor, McDermott, SNC Lavalin and even Worley struggling with this new energy scenario, which cannot sustain these huge organisations.” KBR could fully exit the energy business within 24 months, according to the expert. Pointing to some figures to highlight the issue, company reports show KBR’s backlog in its government segment has increased by 26% since the end of 2017 while Energy Solutions has seen its backlog decline by 17% over the same period.

Fluor is another major player feeling the pressure of large fixed-cost projects. A former Fluor senior manager said energy is the business unit sparking the most concern at present while power, its “shining star” for many years, is being consolidated into infrastructure in a “clear sign of de-risking”. By contrast, government work, with its more steady and consistent revenue streams, “leads the charge”.

Meanwhile, we’re told Jacobs Engineering, although it has less exposure to oil and gas, is busy offsetting costs and improving efficiencies through digital transformation. “The entire E&C market is changing dramatically. It’s no longer sufficient to be concrete and steel experts, where civil and mechanical and structural engineers drive the business,” a former C-level executive at the company said. Firms must now be able to integrate digital technologies into the built environment organically rather than relying on outside partners. Capital project clients have typically procured digital infrastructure as a separate endeavour, but with buying patterns now changing, E&C players must be “digitally fluent”.

“What you’re seeing in the space today is companies doing two things; first, they’re investing in digital technology capabilities and, second, a lot of them, particularly in the US, are investing in their public sector business,” the specialist continued. Specifically, capabilities in digital sensing, remote monitoring, data analytics and cybersecurity are paramount. Those firms that can leverage technology to help clients maximise the potential of their existing infrastructure, or build infrastructure that is safer, more sustainable and cost-effective, will stand out in the crowd. “The companies who ‘get this’ are redefining themselves, not as E&C companies, but as digital solution companies,” the former Jacobs executive said.

Despite all these shifts, energy projects are far from over. Oil and gas has been at the front of the firing line as one of the riskiest sectors to operate in, but remains a significant market. As the liquefied natural gas market recovers, one of the aforementioned experts said a “glut” of projects — totalling over USD 8bn — in the US could come online.

Meanwhile, with COVID-19 shifting project timelines and impacting labour and employment, digital transformation is taking centre stage as companies seek to reduce costs and establish smarter ways of working. We’re told that “the E&C moniker is becoming outdated”, with companies in the technology services space starting to “look and act” differently in response to an array of global trends.

Related Transcripts

The information used in compiling this document has been obtained by Third Bridge from experts participating in Forum Interviews. Third Bridge does not warrant the accuracy of the information and has not independently verified it. It should not be regarded as a trade recommendation or form the basis of any investment decision.

For any enquiries, please contact sales@thirdbridge.com