There were two primary drivers of the price shifts and global nickel demand earlier this year, according to a former EVP from Vale. The first was Chinese steelmaker Tsingshan’s announcement of converting pig nickel capacity into nickel matte. “That had an immediate impact on the market, as the analysts tried to digest what that actually meant for supply and demand,” explained the specialist. The company had agreed to provide 100,000 tonnes of nickel matte to two battery producers, which has knock-on effects for the supply used to make stainless steel.

The second influence was “news around the re-emergence of LFP, lithium iron phosphate, that is used as the battery chemistry for EVs, and this would be in direct competition with the nickel-bearing chemicals such as NCM [nickel, cobalt, manganese].” In fact, this specialist designates LFP a risk in the immediate term. “There have been some developments around pushing up the energy density via technology, primarily around how the cells are packaged.” Consequently, they noted, LFP has become viable for the automotive industry, specifically entry level vehicles.

Tesla’s CEO, Elon Musk, announced late last year that the company would be using LFP batteries within its Model 3 vehicles manufactured in China, citing unreliable long-term nickel supplies. He also explained that this move would free up nickel supplies for other Tesla models. However, LFP has some disadvantages compared with nickel-based batteries. One is the energy density: “There’s still a massive market that’s going to have to be filled once you’re past these smaller, entry-level vehicles that, in my view, cannot be replaced with LFP, simply because the theoretical energy density, which is the maximum energy density that you can achieve from a physics point of view, is limited.”

LFP batteries also perform poorly in colder climates, another specialist explained. The former engineer from Contemporary Amperex Technology Co Ltd (CATL) told Third Bridge Forum that “LFP batteries drain quickly at low temperatures. According to the cell developers, its DCR (direct-current resistance) increases significantly at low temperatures because its ion conduction speed is half that of ternary materials.” As a result, LFP batteries in cold climates can lose their charge overnight.

Within the high nickel content battery category, NCA (nickel, cobalt, aluminate) has a lower cost than NCM batteries, but it presents other issues. For instance, “higher nickel content will enhance the surface activity and produce more residual alkali, so the surface activity needs to be reduced through certain technologies and clever precursors.” In addition, there are more appropriate use-cases for high nickel batteries: “The high nickel content of NCA batteries may cause serious gas generation in the battery. This may not be a big problem for cylindrical batteries because they can withstand the pressure of 0.8-1.2MPa without exploding, but aluminium shell batteries may only withstand 0.4MPa and soft pack batteries even less, so NCA materials are not suitable for the latter two.

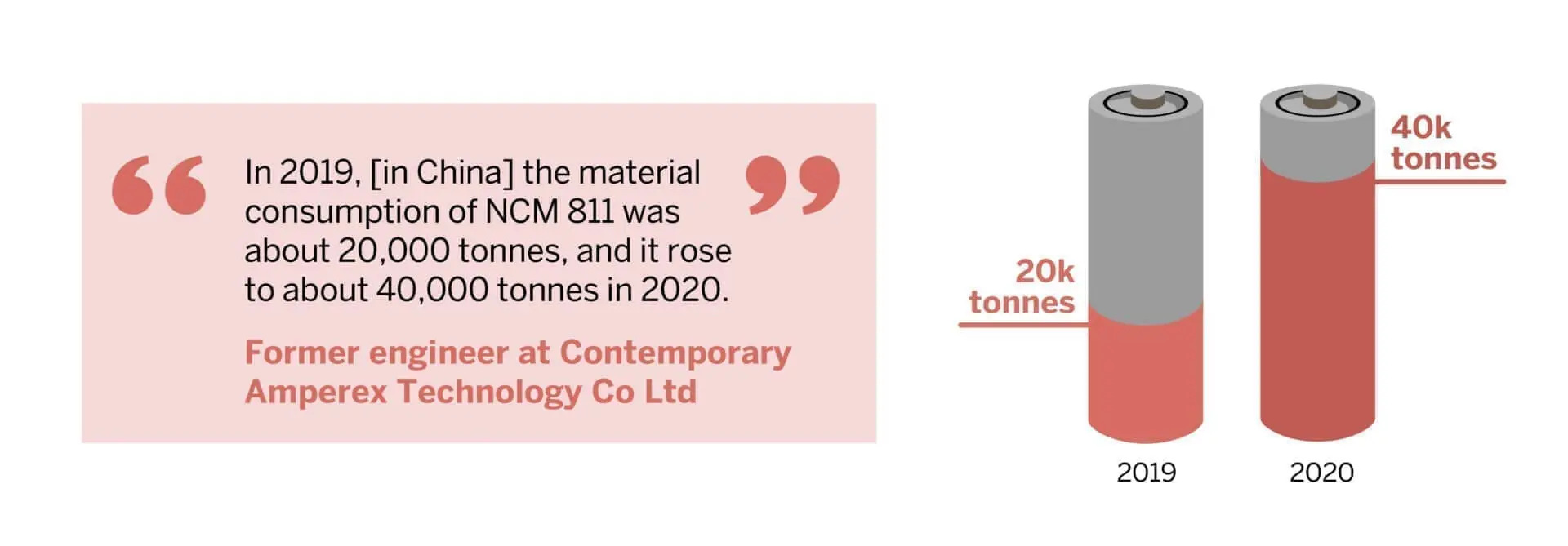

Another notable high nickel variety is NCM 811, which along with NCA batteries, the specialist believes “will account for a big market share in the future”. This is owing to the fact that EVs need a long range such as 400-600km, or even 800-1,000km… Only the high nickel ternary materials or NCA active materials can meet the demand.” Demand for NCM 811 has risen over the past year, the former engineer highlighted: In China alone, “in 2019 the material consumption of NCM 811 was about 20,000 tonnes, and it rose to about 40,000 tonnes in 2020.”

Indeed, China is the world’s leading consumer of nickel, with battery producers concentrated in the country, among other markets in Asia. Meanwhile, Indonesia is the biggest producer of the metal. The country banned exports of nickel ore from January 2020, in a bid to support domestic stainless steel output. However, it can still be exported as part of iron ore, according to Reuters analysts, and as such Indonesia was the second-largest source of nickel for China last year. What’s more, Indonesia looks set to make a move into downstream nickel processing too. Four domestic state-owned enterprises have set up Indonesia Battery Holding, a joint venture. Commenting on whether the new JV will require a foreign partner, a senior executive at Aneka Tambang Tbk PT noted it should be an actor that can “fill their weaknesses”. They also explained that “in order to build the investment in downstream, they should have technology and operation expertise, and market exposure as well, and also the funding itself in order to build the investment.”

While myriad trends are affecting the short-term supply of nickel, there is a concrete move towards EV uptake around the world helping to drive the global nickel demand. With its ability to create durable charges for these vehicles, this commodity looks set to be in demand for the long term.

Related Transcripts

The information used in compiling this document has been obtained by Third Bridge from experts participating in Forum Interviews. Third Bridge does not warrant the accuracy of the information and has not independently verified it. It should not be regarded as a trade recommendation or form the basis of any investment decision.

For any enquiries, please contact sales@thirdbridge.com